Student Loans on Credit Reports

Student loans on credit reports can be the beginning of your credit journey, and if managed correctly can help build an excellent credit history. There are roughly 44 million Americans wandering through the maze known as student loans and combined, they owe over $1.48 trillion in student loan debt. With the average graduate holding more than $37,000 in student loan debt, that is a whole lot of opportunity to build some great credit history.

But student loans on credit reports also open the door to the more scary and harmful prospect of messing up and destroying your credit before you even get it established.

The Good, The Bad and The Dirty

Most of you reading this article are beyond the “establishing” credit stage. You are most likely in the glow of good credit; holding tight to your positive history, or maybe you’re in the middle, regretting a couple hiccups and just hoping you don’t do anything further to damage your credit, OR you are the consumer wading through the bad credit sludge trying to find any way to pull yourself up out of the mess.

No matter where you land on the credit scale, if you have open student loans, there are some important things you should know to help protect your credit along the path to “Paid” status.

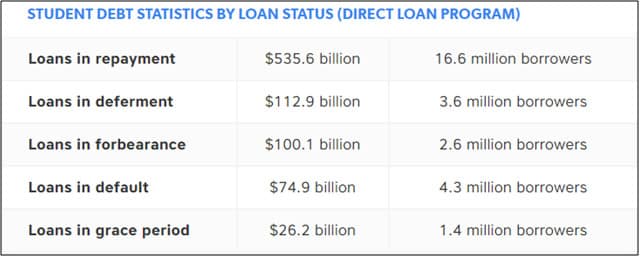

- $1.48 trillion in total U.S. student loan debt

- 44.2 million Americans with student loan debt

- Student loan delinquency rate of 11.2% (90+ days delinquent or in default)

- Average monthly student loan payment: $351 (for borrower aged 20 to 30 years)

- Median monthly student loan payment: $203 (for borrower aged 20 to 30 years)

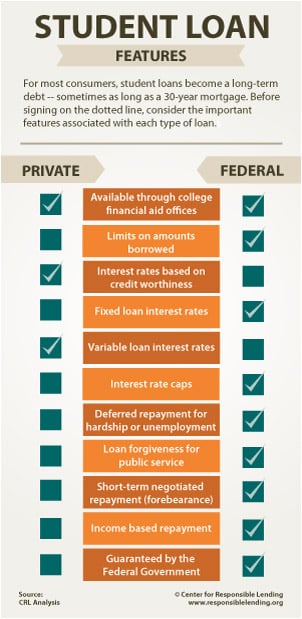

Federal Student Loans vs Private Student Loans

FEDERAL STUDENT LOANS

- Federal student loans are generally fixed interest rates, meaning payments are consistent.

- Federal student loans offer income-driven repayment plans for those struggling to repay their debt. This limits your payment each month based on your income.

- ‘Loan Forgiveness’ for federal student loans may be available after 10 years working in public service. (Currently, there is a bill from House Republicans that could end the Public Service Student Loan Forgiveness program.)

- Most Federal Student Loans have a grace period before repayment starts.

Income-Driven Repayment Plan

- If some or all of your debt is federally guaranteed you could qualify to have your payments capped at 10% – 20% of your income and your payment period stretched to 20-25 years.

- Just remember; the longer you take to pay off, the more you’ll pay in interest.

PRIVATE STUDENT LOANS

- Private Student Loans are held with a private servicer; banks, credit unions, state loan programs or other types of lenders.

- Private student loans do not offer flexible repayment terms or protections provided by the federal government.

- Private student loans offer both fixed or variable interest rates, but they generally have variable interest rates. A variable rate can reset each month or quarter, causing your monthly payments to fluctuate.

- If you are needing payment relief, you must contact the servicer to inquire about any relief they can provide. Some will offer loan modifications or interest rate reductions for struggling borrowers. Some lenders may also temporarily postpone payments to allow you to financially recover.

FEDERAL STUDENT LOAN

- You will not have to start repaying your federal student loans until you graduate, leave school or change your enrollment status to less than half-time.

- The interest rate is fixed and is often lower than private loans – and much lower than some credit card interest rates.

- Undergraduate students with financial need will likely qualify for a subsidized loan where the government pays the interest while you are in school on at least a half-time basis.

- You don’t need a credit check for most federal student loans (except PLUS). Federal Student Loans can help you establish a good credit record.

- Interest may be tax deductible

- Loans can be consolidated into a Direct Consolidation Loan.

- If you are having trouble repaying your loan, you may qualify to temporarily postpone or lower your payments.

- There are several repayment plans, including an option to tie your monthly payment to your income.

- There is NO prepayment penalty fee.

- You may be eligible to have some portion of your loans forgiven if you work in public service.

PRIVATE STUDENT LOAN

- Many private student loans require payments while you are still in school.

- Private student loans can have variable interest rates, some greater than 18%. A variable rate may substantially increase the total amount you repay.

- Private student loans are NOT subsidized, no one will pay the interest on your loan but you.

- Private student loans may require established credit or a co-signer. The cost of private student loans will depend on your credit score and other factors.

- Interest may NOT be tax deductible.

- Loans cannot be consolidated into a Direct Consolidation Loan, but you might be able to find lenders to consolidate your various private student loans.

- Private student loans normally do not offer forbearance or deferment options.

- You should always ask your lender about any repayment options available with a private student loan

- You need to ensure there are no prepayment penalty fees.

- It is unlikely that your lender will offer a loan forgiveness program.

Student Loans on Credit Reports – How Do they Affect Me?

The most important thing to remember is to make your payments on time, every month! Not only will this eliminate the possibility of any additional fees or interest, but it will be reported as positive payment history to the credit bureaus which will improve your credit score, making it easier to obtain credit in the future.

If you get behind on your federal student loan payments and go over 270 days past due, your debt will go into default. At this point, the government can garnish your wages and tax refunds to recoup its money. If this happens, you will also lose access to government programs that can help you pay your debt, such as forbearance and deferment. You also will no longer be eligible for federal student aid in the future. So it’s important for many reasons to take your student loans seriously and stay on top of managing your repayment.

If you are having trouble making your federal student loan payments, you have options.

Let’s explore these options!

Student Loans on Credit Reports – Should you Refinance Them?

Refinancing your Student Loans can be a smart strategy to help lower your interest rate, reduce monthly payments, or otherwise get better terms for your debt. However, you must give them careful thought to ensure you are making the right choice.

- Has your credit score improved since you first applied for your student loans? If so you might be able to get a better interest rate

- Did you originally have a co-signer that needs to be released from your loan? Once you have the credit and income established to hold a loan on your own, you can refinance to release your co-signer from the original loan.

- Some lenders will allow you to combine federal and private student loans into a single loan, this would get you down to one monthly payment with potentially a fixed interest rate. In other words, student loans on credit reports can be combined.

- If you have federal student loans, refinancing could negate some of your options and protections, such as Income Based Repayment Plans, Loan Forgiveness programs and/or Deferment/Forbearance under federal rules. You must be confident you can keep up with your payments now and in the future before giving up these protections.

Most refinance solutions are only beneficial for consumers with “excellent” credit and high income to refinance their private student loans. Refinancing can sometimes help save consumers upwards to $10,000 over the life of the loan.

Consolidating Student Loans

A Direct Consolidation Loan allows you to consolidate multiple federal education loans into one loan. The result is a single monthly payment instead of multiple payments. Once consolidated, you cannot undo and the multiple original federal loans that were a part of the consolidation will be paid off (the original loans should show a zero balance on credit reports).

PROS

-

- Consolidation can greatly simplify your loan repayment reducing it to a single loan with one monthly payment.

- Can lower your monthly payments by getting longer terms to repay your loan.

- Consolidating loans could give you access to additional income-driven repayment plan options that might not have been available on all your various loans.

- Creates consistency by moving variable rate loans to fixed interest rates.

CONS

- Increasing your terms could lead to increased interest paid over the life of the loan.

- Consolidation could cause you to lose certain borrower benefits – such as interest rate discounts, principal rebates or some loan cancellation benefits.

- If you are paying your current loans under an income driven repayment plan or if you’ve made qualifying payments towards Public Service Loan Forgiveness, consolidation will cause you to lose credit for any payments made towards those programs.

There are some requirements for Direct Consolidation Loans:

- Loans must be in “Repayment”.

- Cannot consolidate an existing consolidation loan unless you include an additional eligible loan. FFEL Consolidations have varying circumstances.

- If you want to consolidate a defaulted loan, you must either make satisfactory repayment arrangements (3 consecutive monthly payments) before you consolidate or you must agree to repay your new Direct Consolidation Loan under one of the following:

- Income Based Repayment Plan

- Pay As You Earn Repayment Plan

- Revised Pay As You Earn Repayment Plan

- Income Contingent Repayment Plan

- If you have a defaulted loan that is being collected through garnishment of wages or in accordance with a court order from a judgment, you cannot consolidate the loan unless the wage garnishment has been lifted or the judgment has been vacated.

Most federal student loans, including the following, are eligible for consolidation:

- Federal Stafford Loans – Both subsidized and unsubsidized

- PLUS loans from the Federal Family Education Loan (FFEL) Program

- Supplemental Loans for Students

- Federal Perkins Loans

- Nursing Student Loans

- Nurse Faculty Loans

- Health Professions Student Loans

- Health Education Assistance Loans

- Loans for disadvantaged students

- Direct Subsidized and Unsubsidized Loans

- Direct PLUS Loans

Unless the loans you want to consolidate are in a deferment, forbearance, or grace period, it’s important for you to continue making payments on those loans until your consolidation servicer tells you that they have been paid off by your new Direct Consolidation Loan.

Deferment vs Forbearance – Federal Student Loans

-

- Deferring payments lets you reduce or postpone payments for a somewhat extended length of time. Some common reasons to use deferment:

- Student returning to college.

- Student attending graduate school.

- Taking an internship.

- Completing a residency or fellowship

- Active duty military personnel

Depending on the type of loan you have, you may not have to pay the interest that accrues during a deferment.

Forbearance is for people who are temporarily unable to make payments because of job loss. Forbearance will place a temporary halt on your payments for a limited number of months while you get back on your feet. Interest continues to accrue while your loans are in forbearance, which will increase the amount you pay over the life of the loan. Forbearance is still a better alternative to simply not paying your bill or getting behind on your payments.

Student Loans on Credit Reports – How do they affect my credit?

Your credit scores should not be affected by a deferment or forbearance, however, if you are late or miss a payment prior to being approved for deferment or forbearance, you score would suffer. Be sure to talk with your lenders to explore your options as soon as you think there might be an issue with making payments.